Contents

Poisson vs. Negative Binomial: Modeling Counts and Rates

A practical guide to choosing between Poisson and negative binomial regression for count data. Learn to detect overdispersion, handle excess zeros, and interpret rate ratios correctly.

Quick Hits

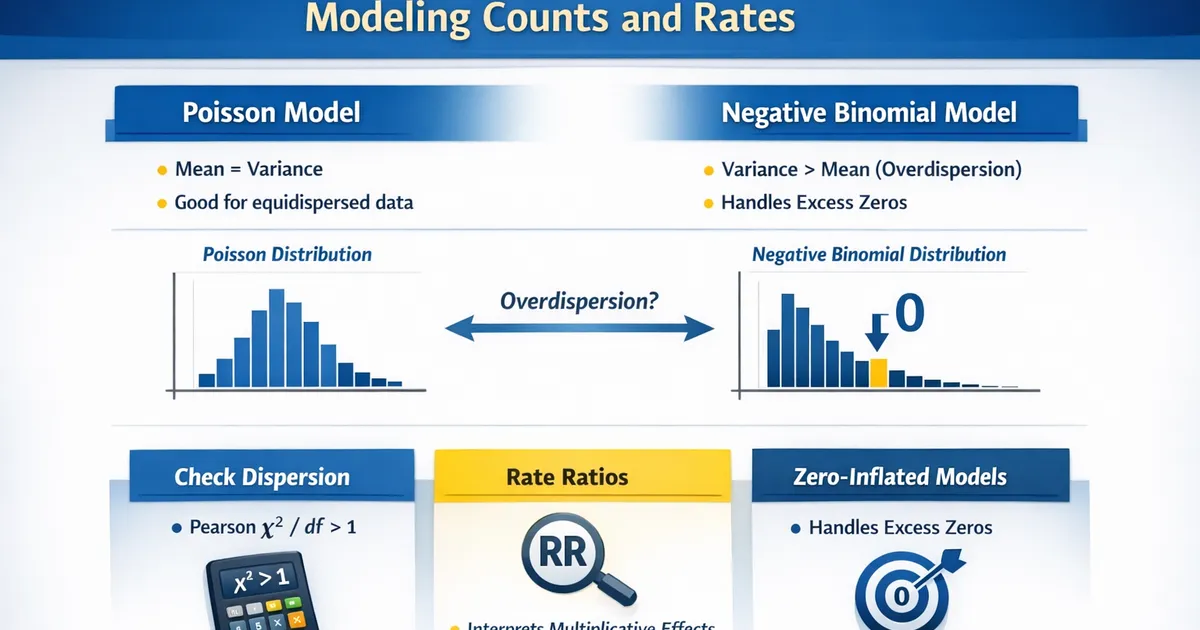

- •Poisson assumes mean equals variance - rarely true in real data

- •Negative binomial allows variance > mean (overdispersion)

- •Check dispersion: Pearson χ²/df >> 1 signals overdispersion

- •Rate ratios interpret as multiplicative changes in expected count

- •Zero-inflated models handle excess zeros from two processes

TL;DR

Count data (purchases, logins, support tickets) requires specialized regression methods. Poisson regression is the standard starting point, but it assumes variance equals the mean—rarely true in practice. When data shows overdispersion (variance > mean), negative binomial regression is preferred. Both produce rate ratios: multiplicative effects on expected counts. This guide shows how to choose between them, diagnose problems, and handle excess zeros.

When to Use Count Models

Use Poisson or negative binomial regression when your outcome is:

- A non-negative integer (0, 1, 2, 3, ...)

- A count of events (purchases, clicks, errors, messages)

- A rate when combined with an exposure/offset (events per time period)

Examples:

- Number of support tickets per user

- Number of purchases per month

- Number of app crashes per session

- Number of logins per week

Don't use when:

- Outcome is continuous → linear regression

- Outcome is binary → logistic regression

- Outcome is bounded (e.g., 0-5 rating) → ordinal regression

Poisson Regression

The Model

Or equivalently:

Key assumption: (variance equals mean)

Interpretation

= rate ratio (RR) for a one-unit increase in

Example: If , then

"For each additional unit of , the expected count is multiplied by 1.49 (a 49% increase)."

Adding an Offset (Exposure)

When observations have different exposure times:

Example: Users observed for different numbers of days

- User A: 10 purchases in 30 days

- User B: 5 purchases in 10 days

Without offset: User A looks more active With offset: User B has higher rate (0.5 vs 0.33 per day)

The Overdispersion Problem

What Is Overdispersion?

Overdispersion occurs when .

Common causes:

- Unobserved heterogeneity (hidden variation between individuals)

- Clustering (events cluster together)

- Correlation between events (one purchase leads to another)

Why It Matters

If you use Poisson with overdispersed data:

- Standard errors are too small

- P-values are too small

- Confidence intervals are too narrow

- You'll find too many "significant" effects

Detecting Overdispersion

Method 1: Dispersion statistic

- : Poisson is fine

-

1.5: Overdispersion likely

-

2: Definite overdispersion

Method 2: Compare mean and variance

For each level of predictors, is variance mean?

Method 3: Formal test

Cameron-Trivedi test for overdispersion:

- H₀: No overdispersion (Poisson is appropriate)

- Reject H₀ → use negative binomial

Negative Binomial Regression

The Model

Same mean structure as Poisson:

But with an extra dispersion parameter (or ):

When , this reduces to Poisson.

Interpretation

Coefficients interpret exactly like Poisson: is the rate ratio.

The difference is in the standard errors—negative binomial accounts for extra-Poisson variation.

When to Use

- Dispersion statistic > 1.5

- Variance clearly exceeds mean

- Likelihood ratio test rejects Poisson

- "To be safe" when you expect heterogeneity

Code: Poisson vs. Negative Binomial

Python

import numpy as np

import pandas as pd

import statsmodels.api as sm

import statsmodels.formula.api as smf

from scipy import stats

def compare_count_models(data, formula, exposure_col=None):

"""

Fit Poisson and Negative Binomial, compare dispersion.

Parameters:

-----------

data : pd.DataFrame

Dataset

formula : str

Model formula (e.g., 'count ~ x1 + x2')

exposure_col : str, optional

Column name for exposure variable (for offset)

Returns:

--------

dict with both models and comparison

"""

results = {}

# Fit Poisson

if exposure_col:

data['log_exposure'] = np.log(data[exposure_col])

poisson_model = smf.poisson(

formula,

data=data,

offset=data['log_exposure']

).fit(disp=0)

else:

poisson_model = smf.poisson(formula, data=data).fit(disp=0)

results['poisson'] = poisson_model

# Calculate dispersion statistic

y_pred = poisson_model.predict()

y_actual = poisson_model.model.endog

pearson_resid = (y_actual - y_pred) / np.sqrt(y_pred)

pearson_chi2 = np.sum(pearson_resid**2)

df_resid = poisson_model.df_resid

dispersion = pearson_chi2 / df_resid

results['dispersion'] = {

'pearson_chi2': pearson_chi2,

'df_residual': df_resid,

'dispersion_ratio': dispersion,

'is_overdispersed': dispersion > 1.5

}

# Fit Negative Binomial

if exposure_col:

nb_model = smf.negativebinomial(

formula,

data=data,

offset=data['log_exposure']

).fit(disp=0)

else:

nb_model = smf.negativebinomial(formula, data=data).fit(disp=0)

results['negative_binomial'] = nb_model

# Likelihood ratio test (Poisson vs NB)

# Under H0: Poisson is adequate, the test statistic is chi-square with df=1

lr_stat = 2 * (nb_model.llf - poisson_model.llf)

lr_pvalue = stats.chi2.sf(lr_stat, 1)

results['lr_test'] = {

'statistic': lr_stat,

'p_value': lr_pvalue,

'prefer_nb': lr_pvalue < 0.05

}

# Model comparison

results['comparison'] = pd.DataFrame({

'Metric': ['Log-Likelihood', 'AIC', 'BIC'],

'Poisson': [poisson_model.llf, poisson_model.aic, poisson_model.bic],

'Neg. Binomial': [nb_model.llf, nb_model.aic, nb_model.bic]

})

return results

def get_rate_ratios(model, confidence=0.95):

"""Extract rate ratios with confidence intervals."""

alpha = 1 - confidence

z = stats.norm.ppf(1 - alpha/2)

coef = model.params

se = model.bse

rate_ratios = pd.DataFrame({

'Variable': coef.index,

'Coefficient': coef.values,

'Rate Ratio': np.exp(coef.values),

'RR CI Lower': np.exp(coef.values - z * se.values),

'RR CI Upper': np.exp(coef.values + z * se.values),

'P-value': model.pvalues.values

})

return rate_ratios

def check_zero_inflation(data, outcome_col):

"""

Check if data has excess zeros beyond Poisson expectation.

"""

y = data[outcome_col]

n = len(y)

mean_y = y.mean()

# Observed zero proportion

obs_zeros = (y == 0).sum() / n

# Expected zeros under Poisson

exp_zeros = np.exp(-mean_y)

return {

'observed_zero_proportion': obs_zeros,

'expected_zero_proportion_poisson': exp_zeros,

'excess_zeros': obs_zeros > exp_zeros * 1.5,

'ratio': obs_zeros / exp_zeros if exp_zeros > 0 else np.inf

}

# Example usage

if __name__ == "__main__":

np.random.seed(42)

n = 500

# Generate overdispersed count data

# Using negative binomial to simulate

from scipy.stats import nbinom

data = pd.DataFrame({

'segment': np.random.choice(['A', 'B', 'C'], n),

'days_active': np.random.uniform(7, 90, n),

'has_premium': np.random.binomial(1, 0.3, n)

})

# Generate counts with overdispersion

mu = np.exp(0.5 + 0.3 * data['has_premium'] + 0.01 * data['days_active'])

alpha = 0.5 # Overdispersion

# Parameterize NB with mean mu and dispersion

r = 1/alpha

p = r / (r + mu)

data['purchases'] = nbinom.rvs(r, p)

# Compare models

results = compare_count_models(data, 'purchases ~ has_premium + days_active')

print("Count Model Comparison")

print("=" * 60)

print(f"\nDispersion ratio: {results['dispersion']['dispersion_ratio']:.2f}")

print(f"Overdispersed: {results['dispersion']['is_overdispersed']}")

print(f"\nLR test p-value: {results['lr_test']['p_value']:.4f}")

print(f"Prefer NB: {results['lr_test']['prefer_nb']}")

print("\n" + "=" * 60)

print("Rate Ratios (Negative Binomial):")

print(get_rate_ratios(results['negative_binomial']))

# Check for zero inflation

print("\n" + "=" * 60)

zi = check_zero_inflation(data, 'purchases')

print(f"Zero inflation check:")

print(f" Observed zeros: {zi['observed_zero_proportion']:.1%}")

print(f" Expected (Poisson): {zi['expected_zero_proportion_poisson']:.1%}")

print(f" Excess zeros: {zi['excess_zeros']}")

R

library(tidyverse)

library(MASS) # For glm.nb

library(AER) # For dispersiontest

library(pscl) # For zero-inflated models

compare_count_models <- function(formula, data, exposure_col = NULL) {

#' Compare Poisson and Negative Binomial models

# Fit Poisson

if (!is.null(exposure_col)) {

data$log_exposure <- log(data[[exposure_col]])

poisson_model <- glm(formula, data = data, family = poisson,

offset = log_exposure)

} else {

poisson_model <- glm(formula, data = data, family = poisson)

}

# Dispersion statistic

pearson_chi2 <- sum(residuals(poisson_model, type = "pearson")^2)

df_resid <- poisson_model$df.residual

dispersion <- pearson_chi2 / df_resid

# Formal dispersion test

disp_test <- dispersiontest(poisson_model, trafo = 1)

# Fit Negative Binomial

if (!is.null(exposure_col)) {

nb_model <- glm.nb(formula, data = data, offset = log_exposure)

} else {

nb_model <- glm.nb(formula, data = data)

}

# Likelihood ratio test

lr_stat <- 2 * (logLik(nb_model) - logLik(poisson_model))

lr_pvalue <- pchisq(as.numeric(lr_stat), 1, lower.tail = FALSE)

list(

poisson = poisson_model,

negative_binomial = nb_model,

dispersion = list(

ratio = dispersion,

test_p = disp_test$p.value,

is_overdispersed = dispersion > 1.5 | disp_test$p.value < 0.05

),

lr_test = list(

statistic = as.numeric(lr_stat),

p_value = lr_pvalue,

prefer_nb = lr_pvalue < 0.05

),

comparison = tibble(

Model = c("Poisson", "Neg. Binomial"),

LogLik = c(logLik(poisson_model), logLik(nb_model)),

AIC = c(AIC(poisson_model), AIC(nb_model)),

BIC = c(BIC(poisson_model), BIC(nb_model))

)

)

}

get_rate_ratios <- function(model) {

#' Extract rate ratios with CIs

coef_vals <- coef(model)

se_vals <- summary(model)$coefficients[, "Std. Error"]

ci <- confint(model)

tibble(

Variable = names(coef_vals),

Coefficient = coef_vals,

`Rate Ratio` = exp(coef_vals),

`RR CI Lower` = exp(ci[, 1]),

`RR CI Upper` = exp(ci[, 2]),

`P-value` = summary(model)$coefficients[, "Pr(>|z|)"]

)

}

# Example

set.seed(42)

n <- 500

data <- tibble(

segment = sample(c("A", "B", "C"), n, replace = TRUE),

days_active = runif(n, 7, 90),

has_premium = rbinom(n, 1, 0.3)

) %>%

mutate(

mu = exp(0.5 + 0.3*has_premium + 0.01*days_active),

purchases = rnbinom(n, size = 2, mu = mu) # Overdispersed

)

# Compare

results <- compare_count_models(purchases ~ has_premium + days_active, data)

cat("Count Model Comparison\n")

cat(strrep("=", 60), "\n")

cat(sprintf("Dispersion ratio: %.2f\n", results$dispersion$ratio))

cat(sprintf("Overdispersed: %s\n", results$dispersion$is_overdispersed))

cat(sprintf("\nLR test p-value: %.4f\n", results$lr_test$p_value))

cat(sprintf("Prefer NB: %s\n", results$lr_test$prefer_nb))

cat("\nRate Ratios (Negative Binomial):\n")

print(get_rate_ratios(results$negative_binomial))

Zero-Inflated Models

When Standard Models Fail

Sometimes you have more zeros than Poisson or negative binomial can explain:

Example: Number of purchases per user

- Many users never purchase (true zeros)

- Among purchasers, counts follow a distribution

- Two separate processes generate zeros

Zero-Inflated Poisson (ZIP)

Assumes two processes:

- With probability : always zero (structural zeros)

- With probability : Poisson-distributed counts (sampling zeros possible)

Zero-Inflated Negative Binomial (ZINB)

Same structure, but the count part follows negative binomial.

Code: Zero-Inflated Models

from statsmodels.discrete.count_model import ZeroInflatedPoisson, ZeroInflatedNegativeBinomialP

# Zero-inflated Poisson

zip_model = smf.poisson('count ~ x1 + x2', data=data) # Standard first

# Note: statsmodels ZI models require different specification

# Using R is often easier for ZI models

library(pscl)

# Zero-inflated Poisson

zip_model <- zeroinfl(purchases ~ has_premium + days_active | 1,

data = data, dist = "poisson")

# Zero-inflated Negative Binomial

zinb_model <- zeroinfl(purchases ~ has_premium + days_active | 1,

data = data, dist = "negbin")

# Compare with Vuong test

vuong(zip_model, zinb_model)

When to Use Zero-Inflation

- Observed zeros >> expected zeros under Poisson/NB

- Theoretical reason for two zero-generating processes

- Vuong test suggests ZI model is better

Don't use if:

- Zeros are just low counts (no separate process)

- You don't have theoretical justification

Comparing Rates Across Groups

Rate Ratio Interpretation

If premium users have RR = 1.5:

- Premium users are expected to have 50% more events

- If baseline is 10 events, premium is 15 events

Comparing to a Reference

# In Python: first category is reference by default with C()

model = smf.negativebinomial('count ~ C(segment) + days', data=data).fit()

# Segment A is reference

# C(segment)[T.B] = rate ratio for B vs A

# C(segment)[T.C] = rate ratio for C vs A

Computing Incidence Rates

When you have exposure (time observed):

With an offset, coefficients give rate ratios directly.

Model Selection Decision Tree

START: Count outcome (0, 1, 2, ...)

↓

CHECK: Is there an exposure variable?

├── Yes → Include as offset

└── No → Proceed

↓

FIT: Poisson model

↓

CHECK: Dispersion ratio

├── ≈ 1 → Poisson OK

└── > 1.5 → Overdispersion

↓

FIT: Negative Binomial

↓

CHECK: Excess zeros?

├── No → NB is final model

└── Yes → Consider zero-inflated

↓

FIT: ZIP or ZINB

Compare with Vuong test

Summary Table

| Feature | Poisson | Negative Binomial | Zero-Inflated |

|---|---|---|---|

| Variance assumption | Two processes | ||

| Use when | Overdispersed | Excess zeros | |

| Standard errors | Can be too small | Appropriate | Appropriate |

| Interpretation | Rate ratios | Rate ratios | Two components |

| Complexity | Simple | Moderate | More complex |

Related Methods

- Regression for Analysts (Pillar) - Complete regression framework

- Comparing Rates - Rate comparisons without regression

- Dealing with Zeros - Zero-handling strategies

- Logistic Regression - Binary outcomes

Key Takeaway

For count data, start with Poisson but expect overdispersion. Check the dispersion ratio (Pearson χ²/df)—if it's above 1.5, switch to negative binomial. Both give rate ratios: multiplicative effects on expected counts. If you have more zeros than the model expects and there's a theoretical reason for two processes (never-purchasers vs. occasional-purchasers), consider zero-inflated models. Always interpret rate ratios correctly: RR = 1.5 means 50% more events, not "50% more likely."

References

- https://www.cambridge.org/core/books/regression-analysis-of-count-data/DC2FFD76B9AA7F3D7E62EA22DAC0AFB0

- https://bookdown.org/roback/bookdown-BeyondMLR/

- https://onlinelibrary.wiley.com/doi/10.1002/sim.3783

- Cameron, A. C., & Trivedi, P. K. (2013). Regression analysis of count data (2nd ed.). Cambridge University Press.

- Roback, P., & Legler, J. (2021). Beyond multiple linear regression: Applied generalized linear models and multilevel models in R. CRC Press.

- Hilbe, J. M. (2011). Negative binomial regression (2nd ed.). Cambridge University Press.

Frequently Asked Questions

When should I use Poisson vs. negative binomial?

What is overdispersion and why does it matter?

How do I interpret rate ratios?

Key Takeaway

Poisson regression is the starting point for count data, but overdispersion is common. Always check dispersion and use negative binomial when variance exceeds the mean. Both give rate ratios, which are multiplicative effects on expected counts.