Contents

Linear Regression Assumptions and Diagnostics in Practice

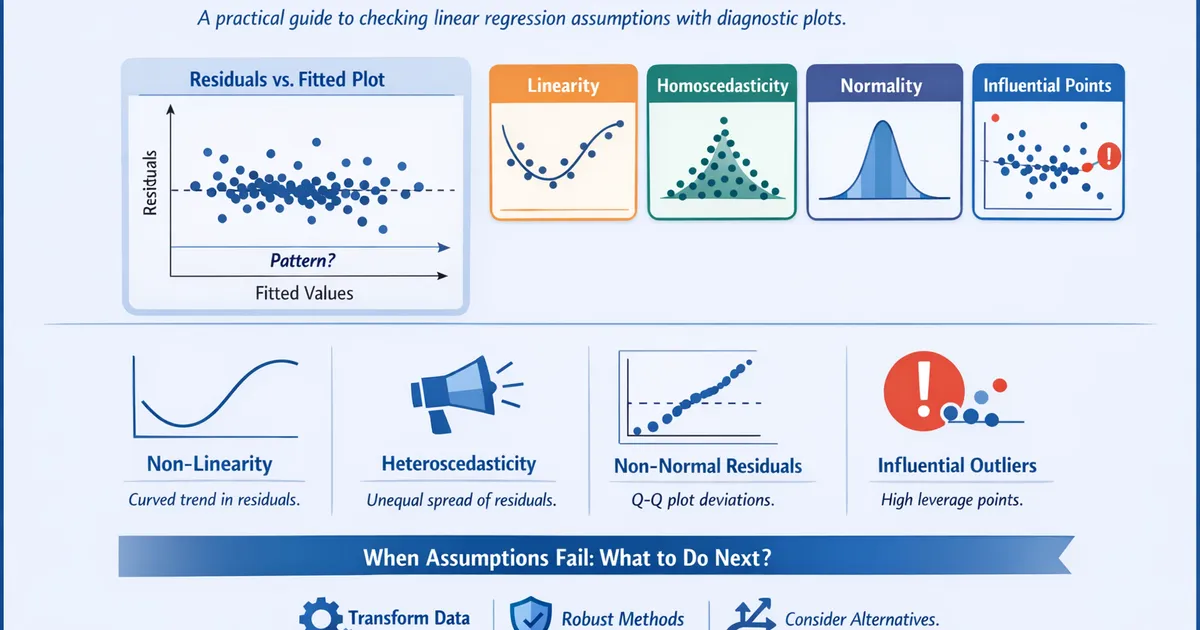

A practical guide to checking linear regression assumptions with diagnostic plots. Learn what violations actually look like, when they matter, and what to do when assumptions fail.

Quick Hits

- •Linearity and homoscedasticity violations are serious - they bias coefficients or standard errors

- •Normality violations are often minor - especially with large samples

- •Independence is the hardest to check and most damaging when violated

- •One influential point can completely change your conclusions

- •Always plot residuals vs. fitted before interpreting any regression

TL;DR

Linear regression makes assumptions about your data. When assumptions hold, coefficients are unbiased and standard errors are correct. When they fail, you may have wrong answers and misleading p-values. This guide shows you how to diagnose violations using residual plots, explains when violations actually matter, and provides practical fixes. The key insight: always check residuals vs. fitted before trusting your results.

The Four Core Assumptions

Linear regression assumes:

- Linearity: The relationship between predictors and outcome is linear

- Independence: Observations are independent of each other

- Homoscedasticity: Variance of residuals is constant across fitted values

- Normality: Residuals are normally distributed

Memory device: LINE (Linearity, Independence, Normality, Equal variance)

What Happens When Assumptions Fail

| Assumption | Violation Effect | Consequence |

|---|---|---|

| Linearity | Biased coefficients | Wrong conclusions about relationships |

| Independence | Understated standard errors | Too many false positives |

| Homoscedasticity | Inefficient estimates, wrong SEs | Unreliable confidence intervals |

| Normality | Unreliable p-values and CIs | (Minor with large n) |

Diagnostic Plot 1: Residuals vs. Fitted

What it shows: Linearity and homoscedasticity

What to look for:

- Random scatter around zero = good

- Curved pattern = non-linearity

- Funnel shape = heteroscedasticity

Good Pattern

| * *

| * * * *

0 -|--*--*--*--*--*--

| * * *

| * * *

+------------------

Fitted Values

Random scatter, no pattern, consistent spread.

Bad: Non-Linearity

| ***

| ***

0 -|------*------

| ***

|***

+------------------

Fitted Values

Curved pattern indicates missing quadratic or other non-linear terms.

Bad: Heteroscedasticity

| *

| * * *

0 -|-*-*-*----*---*---

| * * * *

| * *

+------------------

Fitted Values

Fan shape: variance increases with fitted values.

Diagnostic Plot 2: Q-Q Plot

What it shows: Normality of residuals

What to look for:

- Points following the diagonal line = normal

- S-shape = heavy tails

- Curved away from line at one end = skewness

Good Pattern

Points lie approximately on the diagonal line, with perhaps minor deviations at the tails.

Bad: Heavy Tails

+

+ |

+ |

+ |

+ | <- Points above line at right

|

| <- Points below line at left

More extreme values than normal distribution predicts.

Bad: Skewness

| ++++++

| ++

| ++

|+

+|

++ |

++ |

Asymmetric distribution of residuals.

Diagnostic Plot 3: Scale-Location

What it shows: Homoscedasticity (same as residuals vs. fitted, different view)

Plots: vs. Fitted Values

What to look for:

- Horizontal band = constant variance

- Upward trend = variance increases with fitted values

- Downward trend = variance decreases with fitted values

Diagnostic Plot 4: Residuals vs. Leverage

What it shows: Influential observations

Key concepts:

- Leverage: How unusual is an observation's predictor values?

- Residual: How far is the observation from the prediction?

- Cook's Distance: Combined influence (leverage × residual)

What to look for:

- High leverage + high residual = problematic

- Points beyond Cook's distance contours (usually 0.5 or 1) need investigation

Code: Complete Diagnostic Workflow

Python

import numpy as np

import pandas as pd

import statsmodels.api as sm

import statsmodels.formula.api as smf

from statsmodels.stats.diagnostic import het_breuschpagan, linear_rainbow

from statsmodels.stats.stattools import durbin_watson

from scipy import stats

import matplotlib.pyplot as plt

def comprehensive_diagnostics(model, data, figsize=(14, 12)):

"""

Run complete regression diagnostics.

Parameters:

-----------

model : statsmodels RegressionResults

Fitted OLS model

data : pd.DataFrame

Original data

Returns:

--------

dict with diagnostic results and flags

"""

n = len(model.resid)

# Extract diagnostic quantities

fitted = model.fittedvalues

residuals = model.resid

influence = model.get_influence()

standardized_resid = influence.resid_studentized_internal

leverage = influence.hat_matrix_diag

cooks_d = influence.cooks_distance[0]

# Statistical tests

diagnostics = {}

# 1. Linearity (Rainbow test)

try:

rainbow_stat, rainbow_p = linear_rainbow(model)

diagnostics['linearity'] = {

'test': 'Rainbow',

'statistic': rainbow_stat,

'p_value': rainbow_p,

'flag': rainbow_p < 0.05

}

except:

diagnostics['linearity'] = {'test': 'Rainbow', 'error': 'Could not compute'}

# 2. Homoscedasticity (Breusch-Pagan)

bp_stat, bp_p, _, _ = het_breuschpagan(residuals, model.model.exog)

diagnostics['homoscedasticity'] = {

'test': 'Breusch-Pagan',

'statistic': bp_stat,

'p_value': bp_p,

'flag': bp_p < 0.05

}

# 3. Normality (Shapiro-Wilk, sample if n > 5000)

resid_sample = residuals if n <= 5000 else np.random.choice(residuals, 5000)

shapiro_stat, shapiro_p = stats.shapiro(resid_sample)

diagnostics['normality'] = {

'test': 'Shapiro-Wilk',

'statistic': shapiro_stat,

'p_value': shapiro_p,

'flag': shapiro_p < 0.05

}

# 4. Independence (Durbin-Watson for autocorrelation)

dw_stat = durbin_watson(residuals)

diagnostics['independence'] = {

'test': 'Durbin-Watson',

'statistic': dw_stat,

'interpretation': 'Positive autocorr' if dw_stat < 1.5 else (

'Negative autocorr' if dw_stat > 2.5 else 'No autocorr'),

'flag': dw_stat < 1.5 or dw_stat > 2.5

}

# 5. Influential points

high_leverage_threshold = 2 * (model.df_model + 1) / n

high_leverage = np.sum(leverage > high_leverage_threshold)

high_cooks = np.sum(cooks_d > 4/n)

diagnostics['influential_points'] = {

'high_leverage_count': high_leverage,

'high_cooks_count': high_cooks,

'max_cooks_d': np.max(cooks_d),

'flag': high_cooks > 0

}

# Create diagnostic plots

fig, axes = plt.subplots(2, 2, figsize=figsize)

# Plot 1: Residuals vs Fitted

ax1 = axes[0, 0]

ax1.scatter(fitted, residuals, alpha=0.6, edgecolors='none')

ax1.axhline(y=0, color='red', linestyle='--', linewidth=1)

# Lowess smoothing

from statsmodels.nonparametric.smoothers_lowess import lowess

smooth = lowess(residuals, fitted, frac=0.3)

ax1.plot(smooth[:, 0], smooth[:, 1], 'r-', linewidth=2, label='Lowess')

ax1.set_xlabel('Fitted Values')

ax1.set_ylabel('Residuals')

ax1.set_title('Residuals vs Fitted\n(Check: Linearity, Homoscedasticity)')

# Plot 2: Q-Q Plot

ax2 = axes[0, 1]

stats.probplot(standardized_resid, dist="norm", plot=ax2)

ax2.set_title('Normal Q-Q\n(Check: Normality)')

ax2.get_lines()[0].set_markerfacecolor('steelblue')

ax2.get_lines()[0].set_alpha(0.6)

# Plot 3: Scale-Location

ax3 = axes[1, 0]

sqrt_std_resid = np.sqrt(np.abs(standardized_resid))

ax3.scatter(fitted, sqrt_std_resid, alpha=0.6, edgecolors='none')

smooth = lowess(sqrt_std_resid, fitted, frac=0.3)

ax3.plot(smooth[:, 0], smooth[:, 1], 'r-', linewidth=2)

ax3.set_xlabel('Fitted Values')

ax3.set_ylabel('√|Standardized Residuals|')

ax3.set_title('Scale-Location\n(Check: Homoscedasticity)')

# Plot 4: Residuals vs Leverage

ax4 = axes[1, 1]

ax4.scatter(leverage, standardized_resid, alpha=0.6, edgecolors='none')

ax4.axhline(y=0, color='grey', linestyle='--', linewidth=0.5)

# Cook's distance contours

xlim = ax4.get_xlim()

x_vals = np.linspace(0.001, xlim[1], 100)

for thresh in [0.5, 1.0]:

y_vals = np.sqrt(thresh * n * (1 - x_vals) / x_vals / model.df_model)

ax4.plot(x_vals, y_vals, 'r--', linewidth=0.5, alpha=0.7)

ax4.plot(x_vals, -y_vals, 'r--', linewidth=0.5, alpha=0.7)

ax4.set_xlabel('Leverage')

ax4.set_ylabel('Standardized Residuals')

ax4.set_title('Residuals vs Leverage\n(Check: Influential Points)')

# Annotate highly influential points

for i, (lev, resid, cd) in enumerate(zip(leverage, standardized_resid, cooks_d)):

if cd > 4/n:

ax4.annotate(str(i), (lev, resid), fontsize=8)

plt.tight_layout()

# Summary

flags = []

if diagnostics['linearity'].get('flag'):

flags.append("⚠️ Non-linearity detected (Rainbow test p < 0.05)")

if diagnostics['homoscedasticity']['flag']:

flags.append("⚠️ Heteroscedasticity detected (Breusch-Pagan p < 0.05)")

if diagnostics['normality']['flag']:

flags.append("⚠️ Non-normality detected (Shapiro-Wilk p < 0.05)")

if diagnostics['independence']['flag']:

flags.append(f"⚠️ Autocorrelation detected (DW = {dw_stat:.2f})")

if diagnostics['influential_points']['flag']:

flags.append(f"⚠️ {high_cooks} influential point(s) (Cook's d > 4/n)")

return {

'diagnostics': diagnostics,

'flags': flags,

'figure': fig

}

# Example usage

if __name__ == "__main__":

np.random.seed(42)

n = 200

# Create data with some issues

x1 = np.random.normal(0, 1, n)

x2 = np.random.uniform(0, 10, n)

# Non-linear relationship (quadratic)

y = 2 + 3*x1 + 0.5*x2 - 0.2*x1**2 + np.random.normal(0, 1, n)

data = pd.DataFrame({'y': y, 'x1': x1, 'x2': x2})

# Fit linear model (missing quadratic term)

model = smf.ols('y ~ x1 + x2', data=data).fit()

# Run diagnostics

results = comprehensive_diagnostics(model, data)

print("Diagnostic Summary")

print("=" * 50)

for flag in results['flags']:

print(flag)

if not results['flags']:

print("✓ No major assumption violations detected")

plt.show()

R

library(tidyverse)

library(broom)

library(car)

library(lmtest)

comprehensive_diagnostics <- function(model) {

#' Run complete regression diagnostics

n <- length(residuals(model))

p <- length(coef(model))

# Calculate diagnostic quantities

resids <- residuals(model)

std_resids <- rstandard(model)

fitted_vals <- fitted(model)

leverage <- hatvalues(model)

cooks <- cooks.distance(model)

# Statistical tests

results <- list()

# 1. Linearity (Rainbow test)

rainbow_test <- tryCatch({

lmtest::raintest(model)

}, error = function(e) NULL)

if (!is.null(rainbow_test)) {

results$linearity <- list(

test = "Rainbow",

statistic = rainbow_test$statistic,

p_value = rainbow_test$p.value,

flag = rainbow_test$p.value < 0.05

)

}

# 2. Homoscedasticity (Breusch-Pagan)

bp_test <- lmtest::bptest(model)

results$homoscedasticity <- list(

test = "Breusch-Pagan",

statistic = bp_test$statistic,

p_value = bp_test$p.value,

flag = bp_test$p.value < 0.05

)

# 3. Normality (Shapiro-Wilk)

resid_sample <- if (n > 5000) sample(resids, 5000) else resids

sw_test <- shapiro.test(resid_sample)

results$normality <- list(

test = "Shapiro-Wilk",

statistic = sw_test$statistic,

p_value = sw_test$p.value,

flag = sw_test$p.value < 0.05

)

# 4. Independence (Durbin-Watson)

dw_test <- lmtest::dwtest(model)

results$independence <- list(

test = "Durbin-Watson",

statistic = dw_test$statistic,

p_value = dw_test$p.value,

flag = dw_test$p.value < 0.05

)

# 5. Influential points

high_leverage_thresh <- 2 * p / n

results$influential <- list(

high_leverage_count = sum(leverage > high_leverage_thresh),

high_cooks_count = sum(cooks > 4/n),

max_cooks = max(cooks),

flag = sum(cooks > 4/n) > 0

)

# Generate flags

flags <- c()

if (results$linearity$flag) {

flags <- c(flags, "⚠️ Non-linearity detected (Rainbow test)")

}

if (results$homoscedasticity$flag) {

flags <- c(flags, "⚠️ Heteroscedasticity detected (Breusch-Pagan)")

}

if (results$normality$flag) {

flags <- c(flags, "⚠️ Non-normality detected (Shapiro-Wilk)")

}

if (results$independence$flag) {

flags <- c(flags, "⚠️ Autocorrelation detected (Durbin-Watson)")

}

if (results$influential$flag) {

flags <- c(flags, sprintf("⚠️ %d influential point(s) detected",

results$influential$high_cooks_count))

}

list(

tests = results,

flags = flags

)

}

plot_diagnostics_enhanced <- function(model) {

#' Create enhanced diagnostic plots

par(mfrow = c(2, 2))

# Standard plots with better formatting

plot(model, which = 1, main = "Residuals vs Fitted\n(Check: Linearity, Homoscedasticity)")

plot(model, which = 2, main = "Normal Q-Q\n(Check: Normality)")

plot(model, which = 3, main = "Scale-Location\n(Check: Homoscedasticity)")

plot(model, which = 5, main = "Residuals vs Leverage\n(Check: Influential Points)")

par(mfrow = c(1, 1))

}

# Example usage

set.seed(42)

n <- 200

data <- tibble(

x1 = rnorm(n),

x2 = runif(n, 0, 10)

) %>%

mutate(y = 2 + 3*x1 + 0.5*x2 - 0.2*x1^2 + rnorm(n))

# Fit model (missing quadratic)

model <- lm(y ~ x1 + x2, data = data)

# Run diagnostics

results <- comprehensive_diagnostics(model)

cat("Diagnostic Summary\n")

cat(strrep("=", 50), "\n")

if (length(results$flags) > 0) {

for (flag in results$flags) {

cat(flag, "\n")

}

} else {

cat("✓ No major assumption violations detected\n")

}

# Plot

plot_diagnostics_enhanced(model)

What To Do When Assumptions Fail

Non-Linearity Detected

Options:

- Add polynomial terms:

y ~ x + I(x^2) - Add interaction terms:

y ~ x1 * x2 - Transform predictors:

y ~ log(x) - Use splines or GAMs for flexible non-linearity

# Adding polynomial term

model_quad = smf.ols('y ~ x1 + I(x1**2) + x2', data=data).fit()

Heteroscedasticity Detected

Options:

- Use robust standard errors (doesn't fix inefficiency, does fix SEs)

- Transform the outcome (log transformation common for positive data)

- Use weighted least squares

- Use a generalized linear model with appropriate variance function

# Robust standard errors

from statsmodels.stats.sandwich_covariance import cov_hc3

robust_cov = cov_hc3(model)

robust_se = np.sqrt(np.diag(robust_cov))

Non-Normality Detected

When to worry:

- Small samples (n < 50): May affect CI coverage

- Large samples: Usually fine (CLT)

- Severe skewness: Consider transformation

Options:

- Transform outcome (log, sqrt, Box-Cox)

- Use robust regression (M-estimators)

- Bootstrap for inference

- With large n, often acceptable to proceed

Independence Violated

This is serious. Standard errors are wrong, often too small.

Options:

- Clustered standard errors (cluster at the level of dependency)

- Mixed effects models (for hierarchical data)

- Time series models (for autocorrelated data)

- GEE for repeated measures

# Clustered standard errors

library(sandwich)

library(lmtest)

coeftest(model, vcov = vcovCL(model, cluster = ~group_id))

Influential Points Detected

Steps:

- Identify which observations (check Cook's distance)

- Investigate: Are they data errors? Valid outliers?

- Run analysis with and without them

- Report both results if conclusions differ

- Consider robust regression if outliers are valid but influential

Practical Guidelines: When Violations Matter

Rules of Thumb

| Violation | When It's Serious | When It's Often OK |

|---|---|---|

| Non-linearity | Always problematic | Never OK to ignore |

| Independence | Always problematic | Never OK to ignore |

| Heteroscedasticity | Small samples, prediction intervals | Large samples with robust SEs |

| Non-normality | Small samples (<30) | Large samples, moderate deviations |

Sample Size Buffer

With larger samples, some violations matter less:

- n > 30: Moderate non-normality usually OK

- n > 100: More robust to most violations

- n > 500: Focus mainly on linearity and independence

Effect on Different Quantities

| Quantity | Most Affected By |

|---|---|

| Coefficient estimates | Non-linearity, influential points |

| Standard errors | Heteroscedasticity, independence |

| P-values | All violations (via SEs) |

| Prediction intervals | Heteroscedasticity, non-normality |

| R² | Non-linearity |

The Diagnostic Decision Tree

START: Fit your model

↓

CHECK: Residuals vs Fitted

├── Curved pattern? → Add polynomial terms or transform

├── Funnel shape? → Use robust SEs or transform outcome

└── Random scatter? → Continue

↓

CHECK: Q-Q Plot

├── Severe deviations? + Small sample → Consider transformation

├── Moderate deviations? + Large sample → Usually proceed

└── Points on line? → Continue

↓

CHECK: Leverage/Cook's D

├── High influence points? → Investigate, run sensitivity analysis

└── No issues? → Continue

↓

CHECK: Data structure

├── Clustered/hierarchical? → Use clustered SEs or mixed models

├── Time series? → Check Durbin-Watson, consider time series model

└── Independent? → Continue

↓

PROCEED with interpretation

Related Methods

- Regression for Analysts (Pillar) - Complete regression framework

- Robust Standard Errors - Fixing heteroscedasticity

- Handling Outliers - Robust alternatives

- Transformations Guide - When transforms help

Key Takeaway

Diagnostic plots are more important than the regression output itself. A significant coefficient is meaningless if assumptions are violated and standard errors are wrong. Always check residuals vs. fitted (for linearity and homoscedasticity), Q-Q plots (for normality), and Cook's distance (for influential points). When violations occur, the fix depends on which assumption failed—robust standard errors for heteroscedasticity, polynomials for non-linearity, mixed models for clustering. Never skip diagnostics.

References

- https://www.stat.berkeley.edu/~aldous/157/Papers/Fox.pdf

- https://data.library.virginia.edu/diagnostic-plots/

- https://onlinelibrary.wiley.com/doi/10.1002/sim.3782

- Fox, J. (2015). Applied regression analysis and generalized linear models. Sage Publications.

- University of Virginia Library. Diagnostic plots in R. Research Data Services.

- Williams, M. N., Grajales, C. A. G., & Kurkiewicz, D. (2013). Assumptions of multiple regression. *International Journal of Research & Method in Education*, 36(2), 164-185.

Frequently Asked Questions

Which assumption is most important?

Can I use regression if my data isn't normal?

What's the difference between residual plots and looking at raw data distributions?

Key Takeaway

Regression diagnostics are about checking whether your model captures the systematic patterns in your data and whether your uncertainty estimates are trustworthy. Always plot residuals vs. fitted values first - most problems show up there.